SMM News on June 19:

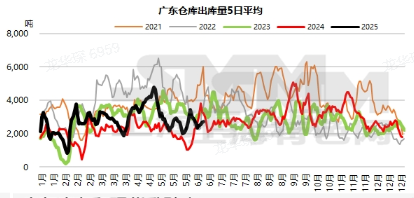

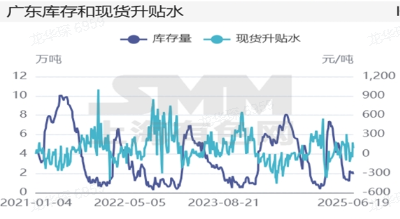

Guangdong region: This week, the premiums and discounts in this region showed a trend of jumping initially and then pulling back. At the beginning of the week, influenced by a relatively large price spread between futures contracts and delivery, spot premiums surged to a premium of 180 yuan/mt after delivery. However, as warrants flowed out and suppliers rushed to liquidate their holdings, premiums continued to decline. As of Thursday, high-quality copper was quoted at a premium of 180 yuan/mt, up 80 yuan/mt from last Thursday. Standard-quality copper was quoted at a premium of 90 yuan/mt, up 70 yuan/mt from last Thursday. SX-EW copper was quoted at a premium of 40 yuan/mt, up 80 yuan/mt from last Thursday. On Thursday, the price spread between premiums and discounts for standard-quality copper in Shanghai and Guangdong was 20 yuan/mt higher in Shanghai, with a relatively small spread, leaving no room for cross-regional cargo transfers. According to SMM statistics, as of Thursday, the total inventory in Guangdong warehouses was 19,200 mt, down 900 mt from last Thursday. The total warrants amounted to 8,600 mt, down 600 mt from last Thursday, with warrants starting to flow into the market after delivery. Specifically: This week, warehouse arrivals were 10,300 mt/week, slightly down 324 mt/week from last week and below the annual average (14,000 mt/week). Both imported copper and domestically produced copper arrivals were relatively low this week. Outflows from warehouses were 11,000 mt/week, down 2,900 mt/week from last week, significantly below the annual average (14,200 mt/week). At the beginning of the week, downstream procurement volume declined before delivery due to a relatively large price spread between futures contracts.

Looking ahead to next week, imported copper arrivals are expected to remain low, and domestically produced copper supply is also expected to decline due to export operations. Regarding downstream consumption, as some downstream enterprises experienced production cuts this week, they are expected to resume normal production next week, with total consumption expected to increase compared to this week. Therefore, we believe that next week will see a decline in supply and an increase in demand, with weekly inventory expected to continue to decline and premiums expected to stabilize and rebound.

》Subscribe to view SMM historical spot metal prices